As part of my effort to add variety to the types of exit planning posts here, I will occasionally include “Second Act”, stories about business owners who have already left one career, and are now doing something else.

The Second Act

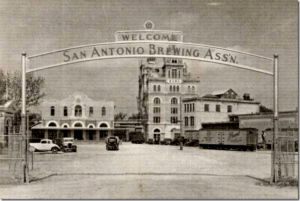

The 19th century Pearl Brewery exemplified both the potential and the problems of close-in urban industrial sites. Long abandoned, but just a mile or so along the river from the famed San Antonio Riverwalk, it was in the words of one real estate agent (quoted from the San Antonio Express-News):

“…an overgrown creek full of homeless encampments. There was terrible crime in the area, and the ground had massive hydrocarbon problems. The buildings were full of asbestos and lead paint, and some were structurally questionable.”

Located next to the major north-south traffic artery from the airport to downtown, The brewery has now been transformed into what is likely the best industrial redevelopment in the nation.

Located next to the major north-south traffic artery from the airport to downtown, The brewery has now been transformed into what is likely the best industrial redevelopment in the nation.

Christopher “Kit” Goldsbury sold Pace Foods to Campbell’s Soup in 1994. In 2002 he purchased the entire 22-acre Pearl site, announcing that it would be redeveloped as a residential/commercial complex.

His vision far outstripped merely knocking out walls and putting shops in. First, the  brewery equipment, largely heavy iron fixtures from the early 20th century, was stripped out, inventoried and stored. Every project in the redevelopment integrates the equipment as a centerpiece, lending a cool steampunk feel to the restaurants and public areas.

brewery equipment, largely heavy iron fixtures from the early 20th century, was stripped out, inventoried and stored. Every project in the redevelopment integrates the equipment as a centerpiece, lending a cool steampunk feel to the restaurants and public areas.

He also sent crews through Texas, locating contemporary buildings made with the same yellow bricks, so they could be disassembled and used to match the existing masonry in buildings being restored.

The residences, however, are all brand new, and command the highest rents in the city. Today, a dozen unique restaurants (the complex has a “no-chains” policy for retail) surround the Emma, a 5-star boutique hotel, and the Culinary Institute of America.

A Vision with Influence

Using the proceeds from the sale of a successful business to create another successful business is admirable, but not unheard of. Doing it in a way that changes an entire city is something else again.

Spurred by The Pearl, the city has extended the Riverwalk north to the complex, with a linear park, art installations and locks to lift the tourist barges to the level of the river’s terminus. Museums and downtown venues are now a 20 minute walk away.

On the “inland” side along Broadway and across the river, other developers have put up new apartments whose chief attraction is “within walking distance of The Pearl.” Another developer is planning a similar complex (18 acres) directly across the street.

On the “inland” side along Broadway and across the river, other developers have put up new apartments whose chief attraction is “within walking distance of The Pearl.” Another developer is planning a similar complex (18 acres) directly across the street.

Spurred by this successful example of “close-in” living for young professionals, mixed multi-family/commercial development is now underway or in the planning stages for tracts of 8, 15 and 20 acres in and around downtown.

Of course, The Pearl has been quietly purchasing adjacent land for years, and will eventually add roughly 50% to its current footprint.

In the next decade, we are likely to see San Antonio complete the transition from a typical modern office-dominated downtown served by sprawling suburbs to one of the most livable inner cities in the nation.

It Takes a Village

Kit Goldsbury isn’t driving all this development personally. He had a cooperative city government, pent up demand for close-in urban-style living, and plenty of money. There are others who have stepped up, both out of a love for San Antonio and from the lure of opportunity.

I’m working on a presentation for a national conference in September. It focuses on the challenge of helping Boomers think about life after the business. So many see a void; an aimless drifting without the anchor of their companies.

You may not have the financial resources of a Kit Goldsbury, but you will always have the vision, the problem-solving ability and the tenacity that made your business successful. That doesn’t go away when you exit. You just need to plan a second act that puts them to good use.

“Read” my new book in 12 minutes!

Your Exit Map, Navigating the Boomer Bust is now available on Amazon, Barnes & Noble and wherever books are sold. It was ranked the #1 new release in its category on Amazon, and is supplemented by free tools and educational materials at www.YourExitMap.com.

Your Exit Map, Navigating the Boomer Bust is now available on Amazon, Barnes & Noble and wherever books are sold. It was ranked the #1 new release in its category on Amazon, and is supplemented by free tools and educational materials at www.YourExitMap.com.

Now, we have a really cool 12 minute animated video from our friends at readitfor.me that summarizes the book, and helps you understand why it is so different from “how to” exit planning tomes. Take some time to check it out here. Thanks!

It will absolutely be an issue if your growth rate falters during due diligence. It’s hard to go through the machinations of a transaction and pay attention to driving the company at the same time. Just be aware that taking your foot off the gas will be noticed, and accounted for.

It will absolutely be an issue if your growth rate falters during due diligence. It’s hard to go through the machinations of a transaction and pay attention to driving the company at the same time. Just be aware that taking your foot off the gas will be noticed, and accounted for. The first is accrued vacation or PTO. It is customary to keep records of this liability off the balance sheet, but professional buyers don’t see it that way. The benefit was earned while producing for the seller. They buyer has no reason to pay it out for work that wasn’t done for him.

The first is accrued vacation or PTO. It is customary to keep records of this liability off the balance sheet, but professional buyers don’t see it that way. The benefit was earned while producing for the seller. They buyer has no reason to pay it out for work that wasn’t done for him. Dini says that many owners “hand off” their companies without a real succession plan, especially when the business is destined to stay in the family. In those cases, ownership is often passed on while control remains—officially or unofficially—in the hands of the original owner, which can cause significant problems.

Dini says that many owners “hand off” their companies without a real succession plan, especially when the business is destined to stay in the family. In those cases, ownership is often passed on while control remains—officially or unofficially—in the hands of the original owner, which can cause significant problems.