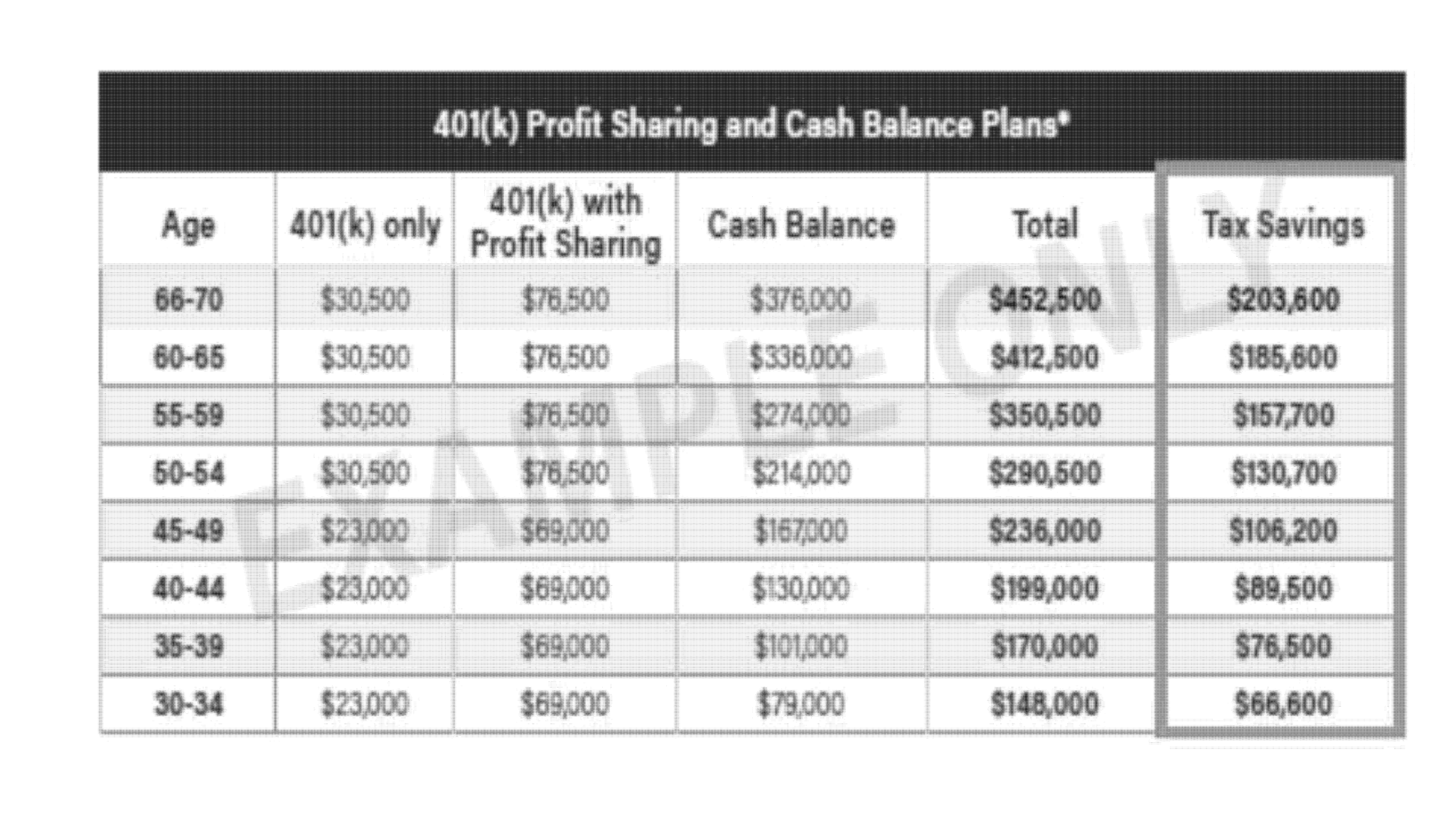

Depending on who you are talking to, Private Equity is either the Great Satan or the savior of small and mid-market companies in the United States. The stories depend a lot on the personal experience of the speakers.

Once a vehicle for high-risk investment plays in corporate takeovers (see Bryan Burrough’s Barbarians at the Gate,) Private Equity has morphed into tranches where specialists seek opportunities in everything from a Main Street entrepreneurship to multi-billion-dollar entities.

What is Private Equity?

The term itself is relatively generic. According to Pitchbook, there are currently 17,000 Private Equity Groups (or PEGs) operating in the US. The accepted business model for our purposes is a limited partnership that raises money to invest in closely held companies. The purpose is plain. Well-run private businesses typically produce a better return on investment than publicly traded entities.

The current Price to Earnings (or PE – just to be a little more confusing) ratio of the S&P 500 is about 27.5. This is after a long bull market has raised stock prices considerably. The ratio is up 11.5% in the last year. That means the average stock currently returns 3.6% profit on its price. Of course, the profits are not usually distributed to the shareholders in their entirety.

Compare that to the 18% to 25% return many PEGs promise their investors. It’s easy to see why they are a favorite of high net worth individuals, hedge funds and family offices. As the Private Equity industry has matured and diversified, they have even drawn investment from the usually more conservative government and union pension funds.

Private Equity Types

Among those 17,000 PEGs the types range from those who have billions in “dry powder” (investable capital,) to some who claim to know of investors who would probably put money into a good deal if asked. Of course, which type of PEG you are dealing with is important information for an owner considering an offer.

The “typical” PEG as most people know it has a fund for acquisitions. It may be their first, or it may be the latest of many funds they’ve raised. This fund invests in privately held businesses. Traditionally PEGs in the middle market space would only consider companies with a free cash flow of $1,000,000 or greater. That left a plethora of smaller businesses out of the game.

The “typical” PEG as most people know it has a fund for acquisitions. It may be their first, or it may be the latest of many funds they’ve raised. This fund invests in privately held businesses. Traditionally PEGs in the middle market space would only consider companies with a free cash flow of $1,000,000 or greater. That left a plethora of smaller businesses out of the game.

For a dozen years I’ve been writing about the pending flood of exiting Boomers faced with a lack of willing and able buyers. I should have known better. Business abhors a vacuum.

Searchfunders

Faced with an overabundance of sellers and a dearth of capable buyers, Private Equity spawned a new model to take advantage of the market, the Searchfunders. These are typically younger individuals, many of whom graduated from one of the “EBA” (Entrepreneurship By Acquisition) programs now offered by almost two dozen business schools.

These programs teach would-be entrepreneurs how to seek out capital, structure deals, and conduct due diligence. Some Searchfunders are “funded”, meaning they have investors putting up a stipend for their expenses. Others are “self-funded.” They find a deal, and then negotiate with investment funds to back them financially.

Both PEGs and Searchfunders seek “platform” companies, those that have experienced management or sufficiently strong operational systems to absorb “add-on” or “tuck-in” acquisitions. The costs of a transaction have bumped many seasoned PEGs into $2,000,000 and up as a cash flow requirement. Searchfunders have happily moved into the $500,000 to $2,000,000 market.

In the next article we’ll discuss how PEGs can promise returns that are far beyond the profitability of the businesses they buy.

John F. Dini develops transition and succession strategies that allow business owners to exit their companies on their own schedule, with the proceeds they seek and complete control over the process. He takes a coaching approach to client engagements, focusing on helping owners of companies with $1M to $250M in revenue achieve both their desired lifestyles and legacies.